When Covid-19 first hit, those of us in the real estate industry predicted a collapse ofthe housing market. In just the first two months of the pandemic, 22.4 million Americans lost their jobs, while gross domestic product fell at the fastest rate in modern history in the second quarter. Instead, what unfolded was a transformation of the housing market, fueled by what is call “migration mania.”

For employees in many industries, working remotely during the pandemic effectively has untethered them from their physical offices. Historically, but even more so during the pandemic, those with higher-income jobs are the most likely to work from home. As a result, many of them have chosen to move from more expensive areas of the country to lower-cost metros.

This emergence of buyers relocating to lower-cost markets, paired with low interest rates, limited housing supply, investors looking to make money on the housing upswing and home shoppers caught up in the excitement, mean higher home prices. In the existing market, which represents the bulk of total home sales, prices are up 24 percent nationally from prices in May of last year, according to National Association of Realtors.

But this is not an equal-opportunity boom. The housing rebound has been fueled by buyers whose wealth allowed them to win bidding wars often with a high down payment and a bid over asking price. Those living on local incomes, which are often modest compared with those of relocating newcomers, are losing the ability to buy a home as competition grows and prices rise. In the long run, this means some Americans will be able to build wealth in their homes, leaving the rest behind.

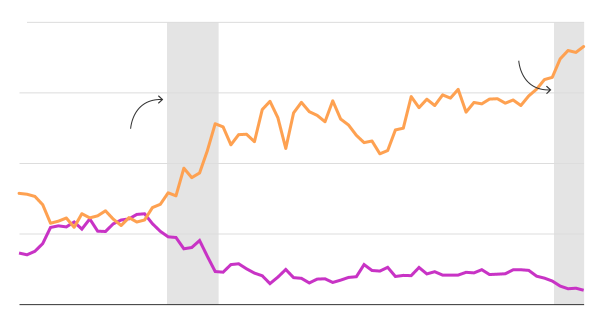

At the onset of the pandemic, buyer confidence crashed. Sales slowed in March 2020, and by May, total transactions were down by 24 percent from the start of the year. Yet May marked the bottom for home sales: Spring 2020 wound up heralding the biggest housing boom in over a decade, helping hundreds of thousands of Americans get back to work. After being cooped up for months, consumers jumped into the market to find their dream house, much to the delight of builders and realtors.

By summer 2020, it became apparent that the demand for housing far exceeded supply, sending prices skyrocketing. In 2019, the median sales price for a home grew 4.9 percent over 2018 levels; by the last six months of 2020, it had jumped to 13.4 percent, according to the realtors’ association.

Soon, wild stories began cropping up from around the country: homes selling for hundreds of thousands of dollars over the asking price, two-year wait lists, realtors holding live auctions, people camping out for days for the chance to buy a new home despite not knowing its price. This frenzy recalls the mid-2000s housing boom — and that, understandably, has people worried.

But today’s market is different. This boom isn’t driven by loose credit and speculative lending. In fact, home buyers today are financially sound, with 73 percent of mortgages in the first quarter of this year going to those with a credit score of at least 760, up from 64 percent last year. Beyond good credit scores, buyers today have healthy debt-to-income ratios and wealth thanks to some combination of savings, home equity, investments and generational transfer.

At the onset of the pandemic, buyer confidence crashed. Sales slowed in March 2020, and by May, total transactions were down by 24 percent from the start of the year. Yet May marked the bottom for home sales: Spring 2020 wound up heralding the biggest housing boom in over a decade, helping hundreds of thousands of Americans get back to work. After being cooped up for months, consumers jumped into the market to find their dream house, much to the delight of builders and realtors.

By summer 2020, it became apparent that the demand for housing far exceeded supply, sending prices skyrocketing. In 2019, the median sales price for a home grew 4.9 percent over 2018 levels; by the last six months of 2020, it had jumped to 13.4 percent, according to the realtors’ association.

Soon, wild stories began cropping up from around the country: homes selling for hundreds of thousands of dollars over the asking price, two-year wait lists, realtors holding live auctions, people camping out for days for the chance to buy a new home despite not knowing its price. This frenzy recalls the mid-2000s housing boom — and that, understandably, has people worried.

But today’s market is different. This boom isn’t driven by loose credit and speculative lending. In fact, home buyers today are financially sound, with 73 percent of mortgages in the first quarter of this year going to those with a credit score of at least 760, up from 64 percent last year. Beyond good credit scores, buyers today have healthy debt-to-income ratios and wealth thanks to some combination of savings, home equity, investments and generational transfer.